Quantifying Tax-Drag Shelter Benefits in Roth Conversions

RMD Reduction and the Hidden Roth Contribution

Executive Summary§

- A Roth conversion involves two distinct planning decisions: whether to convert, and conditional on converting, whether conversion tax should be paid from Inside or Outside assets. These decisions generate two distinct tax-drag shelter (TDS) alphas: RMD-reduction alpha and Synthetic Roth Contribution (SRC) alpha. (§2)

- RMD-reduction alpha arises because conversion reduces future Traditional-account balances and therefore future Required Minimum Distributions (RMDs). Reinvested avoided-RMD dollars remain sheltered rather than compounding in taxable accounts. This benefit exists under both Inside- and Outside-funded conversions. (§5.2)

- SRC alpha arises only under Outside-funded conversions. Paying conversion tax from taxable assets effectively migrates after-tax dollars into the Roth wrapper, creating a Synthetic Roth Contribution. The benefit is the wrapper-migration differential between Roth and taxable growth, not the full future value of the conversion-tax dollars. (§5.1, App A.1)

- Both alphas reduce to the valuation identity , where is sheltered principal and is the per-dollar PV of the yearly sheltered-vs-taxable distribution gap. Embedding SECURE 2.0's bounded owner-life and beneficiary distribution structure is the critical addition that closes the stream and admits closed-form present-value measurement of both alphas. (§3, App A)

- In the worked example, RMD-reduction alpha ($2,522) exceeds SRC alpha ($1,021) because the principal sheltered through reduced future RMDs substantially exceeds the conversion-tax principal generating SRC alpha. (§6)

- Tax-drag shelter contributes ~20% of the additional value beyond the base return in the worked example, and can be separately attributed within conversion IRR — letting planners distinguish drag-avoidance benefits from rate-arbitrage and Medicare effects. (§5.3, §4)

1. Literature Review§

Published treatment of tax drag as a quantified, named PV line item in the Roth-conversion setting is sparse. Five entries illustrate this gap.

McQuarrie & DiLellio (2023), "The Arithmetic of Roth Conversions," Journal of Financial Planning. Equation 4 and Tables 4–5 reinvest after-tax counterfactual RMDs at while the Roth compounds at , establishing that drag compounds rather than accruing linearly. The present paper expands this framework by embedding the full SECURE 2.0 distribution schedule — owner-life RMDs followed by 10-year beneficiary depletion — into the same arithmetic. That bounded schedule is the load-bearing addition: absent a terminal distribution schedule, the after-tax wedge remains open-ended and a breakeven age is the natural output. Closing the schedule at the legally mandated terminus turns the same wedge into a finite cash-flow stream that admits a closed-form PV and an IRR, which is what lets us price RMD-reduction alpha as a separate per-decision line item rather than report it as a breakeven scalar.

Reichenstein & Meyer (2017), "Valuing Roth Conversion and Recharacterization Options," Journal of Financial Planning 30(11): 48–56. Their Strategy 3 (outside-funded conversion) vs Strategy 2 (inside-funded) comparison computes , the drag wedge on the conversion-tax dollars — algebraically what the present paper isolates as SRC alpha. R&M do not extend this to the RMD-reduction channel: the avoided-RMD stream sheltered from drag (the dominant alpha in most conversions) is not separately priced, and the common drag structure linking the two channels is not separately identified. Results are reported as FV ratios at the withdrawal year rather than PV at the conversion year.

Vanguard BETR (Passman, Wong & Dickson 2025). Computes Jill's break-even future tax rate from Roth multiple , taxable multiple , and ; — our equivalent embedded drag (Cheshire 2026, §6). The framings are algebraically identical, yet 23.3% vs. Jill's expected 24% reads as plausible; the equivalent tax-drag rates of 37.5% and 34.95% (from ) may appear less so. Viewed through the present framework, BETR can be re-expressed as an implied tax-drag assumption: the break-even on is algebraically a break-even on , with as the implied figure in Jill's case. The reframing substitutes a future statutory rate for an embedded portfolio-level drag the planner can estimate and influence.

Mike Piper, "The 4 Effects of a Roth Conversion." Names the Outside-payment benefit and the RMD-reduction benefit qualitatively but does not quantify either or produce PV/IRR figures.

Kitces. Acknowledges the Outside-payment benefit and account-level drag qualitatively; does not isolate the conv-tax dollar's counterfactual as a PV or IRR line item.

Across these treatments, tax drag appears as an embedded assumption, breakeven condition, or qualitative benefit — rather than as two separately priced PV alphas corresponding to the planner's two distinct decisions: whether to convert, and conditional on converting, whether to fund the tax from inside or outside assets.

To our knowledge, prior Roth-conversion studies have not reported the drag avoided on the counterfactual reinvestment of eliminated RMDs as a separately priced present-value component of conversion value. The contribution is isolation, quantification, and decision-attribution—not discovery of the underlying drag-compounding mechanism.

2. Tax-Drag Shelter§

Tax-Drag Shelter (TDS) is the present-value gap between holding investments inside vs. outside a tax-advantaged wrapper. Inside, investments grow unencumbered by taxes; outside, the same dollars pay annual tax on dividends, interest, realized capital gains, and turnover-driven distributions — a drag that compounds materially over time.

A Roth conversion can capture this benefit in two ways, each creating positive alpha.

-

RMD-reduction alpha (primary):

All conversions (Inside & Outside) reduce the Traditional account by an amount , causing reduced future RMDs. RMD reductions that would have been reinvested taxably remain sheltered. RMD-reduction alpha is the PV of that sheltering.

-

SRC alpha (secondary):

Outside-funded conversions migrate () after-tax dollars into the Roth wrapper — a hidden Roth contribution, formally a Synthetic Roth Contribution (SRC; Cheshire 2026). SRC alpha is the PV gain of compounding tax-free as it distributes vs. in the taxable counterfactual. Identical alpha accrues to a same-sized statutory Roth contribution.

3. The Drag-Shelter Valuation Identity§

A common process creates both TDS alphas: run two parallel accounts on a shared distribution schedule — one sheltered at , one taxable at — and sum the PV of the yearly distribution gap. For principal , the drag-shelter multiplier is this per-dollar sum (derivation in Appendix A; simulator in Appendix B):

§5 specializes the calculation twice. SRC alpha applies it to principal , distributed on the planner's chosen schedule across owner life and the 10-year beneficiary annuity. RMD-reduction alpha applies it to avoided-RMD dollars that accumulate during owner life, then distribute over the 10-year beneficiary annuity only.

4. Advisor Decision Hierarchy§

A Roth conversion involves two sequential decisions:

- Whether to convert.

- Conditional on converting, whether to pay the tax from Inside or Outside assets.

These decisions create distinct tax-drag shelter alphas:

- Conversion decision → RMD-reduction alpha.

- Outside-settlement decision → SRC alpha.

Because RMD-reduction alpha and SRC alpha can materially affect conversion value, planners who evaluate conversions only through tax-rate arbitrage and Medicare effects may misclassify economically beneficial conversions as unattractive.

5. The Two TDS Alphas§

5.1 SRC alpha — Outside-funded conversions only§

Specializing §3 with ,

Two-stage construction (RMD distribution). Phase 1 (owner-life): compounds in two parallel balances — sheltered at , taxable at — and distributes each year via the RMD divisor. The yearly sheltered-vs-taxable distribution gap accrues as alpha. Phase 2 (beneficiary period): the residual distributes as a 10-year fixed annuity (FA); the same gap mechanic continues. Appendix B.1 gives the construction. (Under FA distribution, Phase 1 is itself a fixed annuity across owner life — no separate Phase 2.)

The conventional Hidden Contribution figure equates the conv-tax dollar's value with its full sheltered-wrapper future value — implicitly assuming it would have done nothing absent conversion. The counterfactual is taxable growth at . The TDS framing extracts only the sheltered-vs-taxable differential as drag-avoidance value, leaving the would-have-grown-anyway portion correctly attributed to the conv-tax dollar regardless of conversion. (Appendix A.1 gives the decomposition.)

Inside payment. No wrapper migration occurs, so .

SRC alpha is the drag-avoidance component of total SRC value; Appendix A.1 splits it from the taxable-side growth term.

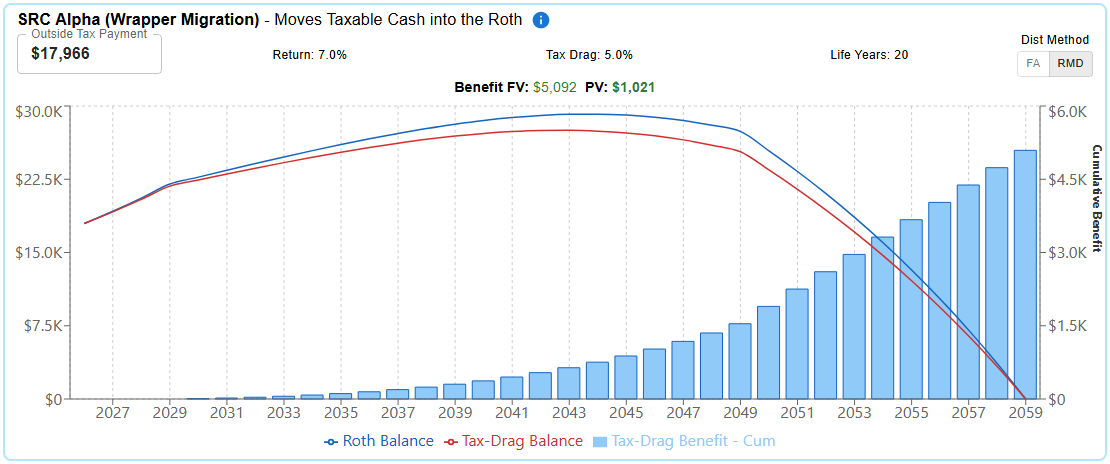

Figure 1. SRC alpha. = $17,966 conversion-tax dollars compound in a sheltered Roth vs. a taxable counterfactual (drag = 5%), distributing under RMD, then FA for beneficiary; the per-year gap accrues PV = $1,021.

5.2 RMD-reduction alpha — Inside- and Outside-funded conversions§

The principal being sheltered is the after-tax converted balance scaled by the reinvestment share, . Specializing §3 on the avoided-RMD schedule,

Because RMD divisors depend on age, not balance, the avoided-RMD stream scales linearly in , justifying the use of the scaling principal in the identity above. The multiplier (Appendix B.2) prices the drag-shelter value per dollar of that scaling principal.

Two-stage construction. Phase 1 (owner-life): each year's avoided RMD enters two parallel balances — sheltered at , taxable at . Nothing distributes; the owner-life drag accumulates in the balance gap. Phase 2 (beneficiary period): under the SECURE-Act 10-year mandate, both balances distribute as a 10-year fixed annuity, and the yearly sheltered-vs-taxable gap delivers the alpha. Phase 2 is identical in structure to SRC alpha's Phase 2.

is the surplus-wealth reinvestment share; consumed RMDs cancel across conversion and counterfactual paths and are out of scope.

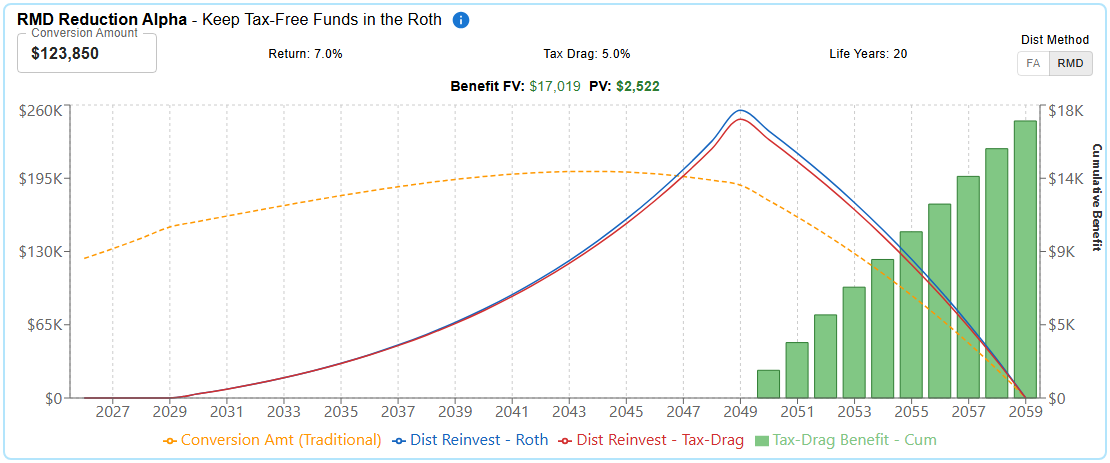

Figure 2. RMD-reduction alpha. Avoided RMDs reinvest in parallel sheltered and taxable balances during Phase 1 (owner life); both distribute as a 10-year fixed annuity in Phase 2 (beneficiary period). Cumulative drag-avoidance benefit reaches PV = $2,522.

Both figures show balances depleting to zero — owner-life RMDs plus SECURE-mandated 10-year beneficiary distribution form a bounded schedule that admits closed-form PV (and IRR for SRC alpha).

5.3 Total TDS alpha§

Under Outside payment,

Under Inside payment, since no wrapper migration occurs and .

Both alphas also feed the conversion's IRR through yearly drag-related cash flows — the SRC flow over owner-life and beneficiary distributions, the RMD-reduction flow over the beneficiary period — so a planner can attribute a quantified share of the deployed IRR to drag avoidance. Appendix C gives the per-year definitions. Under Inside payment (no user outlay) the conversion IRR is undefined and the RMD-reduction PV stands alone.

6. Worked Example§

Converting $123,850 fills through the 22% bracket, with an effective tax rate of 14.5%.

Inputs.

| Parameter | Symbol | Value |

|---|---|---|

| Pre-tax return | 7% | |

| Tax-drag rate | 5% | |

| After-drag return | 6.65% | |

| Conversion principal | $123,850 | |

| Conversion-year effective rate | 14.5% | |

| Conversion tax | $17,966 | |

| Owner remaining life | 23 years (69–92) | |

| Beneficiary period | 10 years | |

| RMD reinvestment | 75% |

The two alphas — Outside- vs. Inside-funded tax payment:

| Component | Outside payment | Inside payment |

|---|---|---|

| RMD-reduction alpha | $2,522 | $2,522 |

| SRC alpha | $1,021 | $0 |

| TDS total | $3,543 | $2,522 |

| Conversion IRR | 11.56% | undefined (no outlay) |

Interpretation. Inside- and Outside-funded conversions both yield $2,522 RMD-reduction alpha. Outside funding adds $1,021 SRC alpha. RMD alpha is 2.47× larger, effectively scaling with $79,419, vs. $17,966 — 4.42×. SRC's smaller principal earns a higher per-dollar multiplier ( vs. ), but not enough to overcome RMD's 4.42× principal advantage.

All Roth conversions produce RMD-reduction alpha while only Outside conversions create SRC alpha. Outside's 11.56% IRR is the 7% base plus rate-arbitrage ($13,280) + Medicare ($1,028) + TDS ($3,543) alphas. TDS contributes 19.8% of that alpha, which may be on the small side: our example's rate-arbitrage alpha is inflated by the Social Security tax-torpedo impact, so typical conversions may have a larger TDS share.

Appendix D gives the per-year RMD and SRC drag flows in nominal and PV terms; §7 shows sensitivity to longer life, higher drag, and reinvestment share.

7. Conclusion§

Three implications for conversion planning.

-

Judge the Conversion decision on RMD-reduction alpha alone. It applies to both Inside- and Outside-funded conversions, scales with and is the dominant TDS alpha.

-

Judge the Outside-settlement decision (paying conversion tax with outside funds) on SRC alpha. It captures the value of moving dollars into the Roth — identical to what a same-sized statutory Roth contribution gains.

-

Attribute, don't aggregate. Reporting a single conversion IRR conflates rate arbitrage, Medicare effects, and drag shelter. The two alphas let a planner show clients which slice of the IRR each decision actually buys, and which assumptions (, , , owner life) drive which slice.

Sensitivity considerations.

| Parameter Change | SRC Alpha | RMD Alpha |

|---|---|---|

| Longer life | ↗ | ↑ |

| Higher drag | ↑ | ↑ |

| Higher RMD reinvestment | — | ↑ |

Magnitude examples (base + parameter variations).

| Scenario | RMD-reduction alpha | SRC alpha | RMD/SRC | TDS total |

|---|---|---|---|---|

| Base (=23, =5%) | $2,522 | $1,021 | 2.47× | $3,543 |

| Longer life (=28) | $3,605 | $1,055 | 3.42× | $4,660 |

| Higher drag (=7%) | $3,495 | $1,410 | 2.48× | $4,905 |

| Both (=28, =7%) | $4,985 | $1,455 | 3.43× | $6,440 |

RMD-reduction alpha is highly time-sensitive: longer life extends Phase 1 accumulation, producing a larger Phase 2 starting balance. SRC alpha is self-limiting: extending Phase 1 distributes more of , shrinking the Phase 2 residual — Phase 1 gains roughly offset Phase 2 shrinkage. For RMD-reduction, and compound: changing both increases alpha by $2,463 — ~$407 more than their individual sum ($1,083 + $973 = $2,056).

Takeaway. Tax-drag shelter is captured predominantly through the RMD-reduction channel — available to both Inside- and Outside-funded conversions — while the wrapper-migration benefit of Outside funding is the smaller, less time-leveraged piece.

Appendix A. The Drag-Avoidance Value Identity§

Notation. The following symbols are used throughout Appendices A–C.

| Symbol | Meaning |

|---|---|

| Sheltered wrapper; compounds at | |

| Unsheltered taxable wrapper; compounds at | |

| Balance at time in each wrapper | |

| Accumulation balance for avoided RMDs (Appendix B.2) | |

| Distribution in year from each wrapper | |

| , the yearly distribution gap | |

| FV factor at horizon : , (no distributions) | |

| , per-dollar PV multiplier | |

| Schedule-specific multipliers (App B); , |

The identity. Place a principal of dollars at into either a sheltered wrapper (compounding at ) or an unsheltered taxable wrapper (compounding at ), and distribute each on a common schedule . The household receives the distribution stream; wrapper choice does not change time-zero outlay. Discounting at , the incremental present value of the sheltered wrapper is

where is the per-dollar multiplier surfaced in §5.

Assumptions. (i) Identical pre-tax return path inside and outside the wrapper. (ii) Identical distribution method and schedule. (iii) Principal enters at time 0; distributions follow per the schedule. (iv) No additional rate effects layered onto the same dollar (no contribution-year vs. distribution-year arbitrage). (v) End-of-period distributions: balances accrue a full year of return before the year's distribution is taken, matching the simulator step order in Appendix B.

Proof sketch. The sheltered balance evolves as with , and the unsheltered counterfactual as with . The household receives the distribution stream and discounts it at . The incremental PV is therefore . Linearity in gives the per-dollar form .

Comment. The identity reduces to two questions: what principal is being sheltered, and what distribution schedule drives ? §5.1 sets on the post-conversion Roth schedule; §5.2 sets on the avoided-RMD schedule.

A.1 SRC alpha within total SRC value§

Let and denote per-dollar future values at horizon in the sheltered and taxable wrappers respectively (no distributions). The Synthetic Roth Contribution's total wealth value (Cheshire 2026) decomposes into two components:

- Taxable-counterfactual growth, — the future value the dollars would have earned at had they remained in the taxable wrapper. This value is properly attributed to the conv-tax dollar regardless of conversion choice.

- Drag-avoidance alpha, — the excess generated by the dollars compounding at inside the Roth rather than at outside. This is the wrapper-migration benefit and is available only inside the Roth.

SRC alpha is the drag-avoidance component: (Appendix B.1 defines ). The conventional Hidden Contribution figure implicitly assumes a zero-growth taxable counterfactual and conflates the two components; the TDS framing extracts only the differential as alpha.

Appendix B. Drag-Shelter Simulator§

Both alphas run a sheltered balance at and an unsheltered counterfactual at on a common distribution schedule, then sum the PV of the yearly gap discounted at . End-of-period convention: a full year of return accrues before the year's distribution is taken (App A assumption (v)).

Annuity factor. , the level annual payment per dollar of starting balance over years at rate .

Distribution methods. RMD applies an age-indexed life-expectancy divisor to the running balance: . FA payments are constant at across years.

B.1 SRC alpha: distribution from K§

Place dollars at in parallel sheltered and unsheltered balances .

Phase 1 — owner-life RMD distribution. For years of the owner's remaining life: distribute and ; update and . The realized gap is the owner-life SRC flow.

Phase 2 — beneficiary 10-year fixed annuity. Hold payments constant at and ; update balances each year.

(Under FA distribution method, Phase 1 is itself a fixed annuity across owner life with no separate Phase 2.)

B.2 RMD-reduction alpha: accumulation before distribution§

Let be the avoided RMD dollars in year — the pre-conversion-minus-post-conversion RMD differential scaled by reinvestment share . Reinvestment balances start at zero.

Phase 1 — owner-life accumulation. For years : compound prior balances at and , then add to each. No distributions, so throughout owner life.

Phase 2 — beneficiary 10-year fixed annuity. Hold payments constant at and ; update balances each year.

The Phase-2 is the RMD-reduction per-year flow used in Appendix C; owner-life entries are zero.

Appendix C. IRR Attribution: Per-Year Drag-Related Cash Flows§

§5.3 reports that the conversion IRR carries a drag-avoidance share. This appendix gives the per-year cash flows behind that claim.

Per-year flows. Let be the yearly sheltered-vs-taxable gap on SRC alpha's two-phase schedule (Appendix B.1), and the analogous Phase-2 gap on RMD-reduction alpha's beneficiary 10-year annuity (Appendix B.2). The conversion's incremental cash flow in year picks up two drag-related terms:

The first runs over the owner's remaining life and beneficiary period; the second is non-zero only in the beneficiary period.

Legitimacy. Both flows exist because of the conversion decisions: disappears under Inside payment by construction; exists only because the conversion reduced the Traditional balance generating RMDs. Discounting at , .

Scope. The conversion IRR is defined only under Outside payment (where is a real outlay). Under Inside payment the IRR is undefined and the RMD-reduction PV is the reportable figure.

Appendix D. Worked Example: Per-Year TDS Cash Flows§

PV discounted at = 7% to 2026.

| Year | RMD drag (nominal) | SRC drag (nominal) | RMD drag PV | SRC drag PV |

|---|---|---|---|---|

| 2026 | — | — | — | — |

| 2027 | — | — | — | — |

| 2028 | — | — | — | — |

| 2029 | — | — | — | — |

| 2030 | — | $8 | — | $6 |

| 2031 | — | $12 | — | $8 |

| 2032 | — | $16 | — | $10 |

| 2033 | — | $20 | — | $13 |

| 2034 | — | $25 | — | $15 |

| 2035 | — | $31 | — | $17 |

| 2036 | — | $37 | — | $19 |

| 2037 | — | $44 | — | $21 |

| 2038 | — | $51 | — | $23 |

| 2039 | — | $60 | — | $25 |

| 2040 | — | $68 | — | $27 |

| 2041 | — | $79 | — | $29 |

| 2042 | — | $89 | — | $30 |

| 2043 | — | $101 | — | $32 |

| 2044 | — | $114 | — | $34 |

| 2045 | — | $127 | — | $35 |

| 2046 | — | $142 | — | $37 |

| 2047 | — | $157 | — | $38 |

| 2048 | — | $172 | — | $39 |

| 2049 | — | $189 | — | $40 |

| 2050 | $1,702 | $355 | $336 | $70 |

| 2051 | $1,702 | $355 | $314 | $65 |

| 2052 | $1,702 | $355 | $293 | $61 |

| 2053 | $1,702 | $355 | $274 | $57 |

| 2054 | $1,702 | $355 | $256 | $53 |

| 2055 | $1,702 | $355 | $239 | $50 |

| 2056 | $1,702 | $355 | $224 | $47 |

| 2057 | $1,702 | $355 | $209 | $44 |

| 2058 | $1,702 | $355 | $195 | $41 |

| 2059 | $1,702 | $355 | $183 | $38 |

| Total | $17,019 | $5,092 | $2,522 | $1,021 |

Em-dash entries reflect accrual without distribution, not zero value. Both alphas accumulate internally before realizing as cash flows: the SRC balance compounds at sheltered vs. taxable rates during gap years 2027–2029, and the avoided-RMD dollars compound in two parallel reinvestment balances throughout owner life (2027–2049). SRC realization begins in 2030 with owner-life RMDs and continues through the beneficiary 10-year annuity (2050–2059); RMD-reduction's full accumulated drag is realized only during the beneficiary period (2050–2059).

PV totals reconcile to the §6 figures. The SRC PV is concentrated in the beneficiary period despite SRC drag accruing throughout owner life because owner-life amounts are small and heavily discounted.

References§

Cheshire, S. M. (2026). The Synthetic Roth Contribution: Empirical and Algebraic Proofs of a Hidden Component in Outside-Funded Roth Conversions. Working paper, SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6772118

Kitces, M. (n.d.). Various articles on asset-location yield-split, tax-diversification, and Roth-conversion mechanics. Available at kitces.com.

McQuarrie, E. F., & DiLellio, J. A. (2023). The arithmetic of Roth conversions. Journal of Financial Planning, 36(5), 72–89. https://www.financialplanningassociation.org/learning/publications/journal/MAY23-arithmetic-roth-conversions-OPEN

Passman, A., Wong, J., & Dickson, J. (2025, July). A BETR Approach to Roth Conversions. Vanguard Research. https://corporate.vanguard.com/content/dam/corp/research/pdf/a_betr_approach_to_roth_conversions_072025.pdf

Piper, M. (n.d.). The 4 effects of a Roth conversion. Oblivious Investor. https://obliviousinvestor.com/the-4-effects-of-a-roth-conversion/ (and related Bogleheads video, Prepay Taxes with Roth Conversions?).

Reichenstein, W., & Meyer, W. (2017, November). Valuing Roth conversion and recharacterization options. Journal of Financial Planning, 30(11), 48–56. https://www.financialplanningassociation.org/sites/default/files/2021-08/NOV17%20Reichenstein.pdf

Acknowledgments§

The author thanks Mike Piper, whose "The 4 Effects of a Roth Conversion" and Bogleheads video "Prepay Taxes with Roth Conversions?" inspired the drag-shelter formalization developed in this paper.